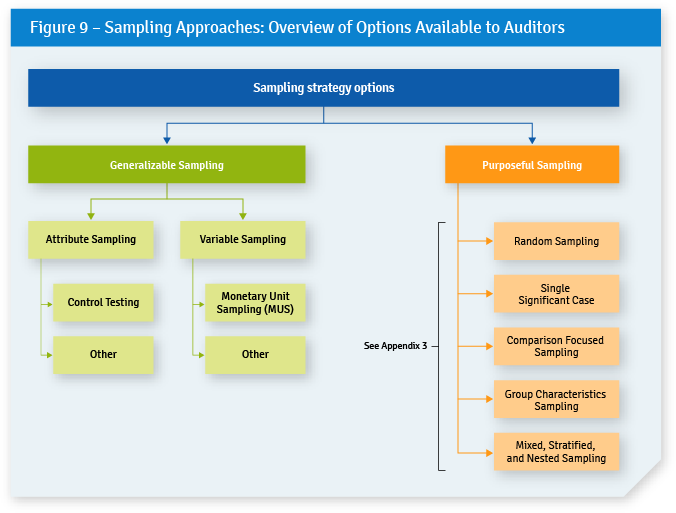

Step 2 – Selecting a Sampling Approach

A very important decision auditors must take once they have determined that they can and will be using sampling to gather audit evidence is whether they should use a generalizable sampling approach or a purposeful sampling approach. This decision is governed by the need to determine which approach best enables the efficient collection of sufficient and appropriate evidence to meet the testing objective.

Selecting the right sampling approach will depend on

- the nature and complexity of the questions auditors need to answer,

- how generalizable to the entire population the sample needs to be,

- the characteristics of the population being studied, and

- the resources available.

This section explores the factors that auditors must take into account to reach this decision. Figure 9 (an expanded version of Figure 5) provides a non-exhaustive overview of the options available to auditors. More methods are in Appendix 2 and Appendix 3.